With only two months remaining before 2025, significant changes to the Central Provident Fund (CPF) system are on the horizon. Announced earlier this year and prior, these updates will impact CPF members, especially those nearing retirement. We’re here to keep you informed and help you understand how these changes may affect your plans.

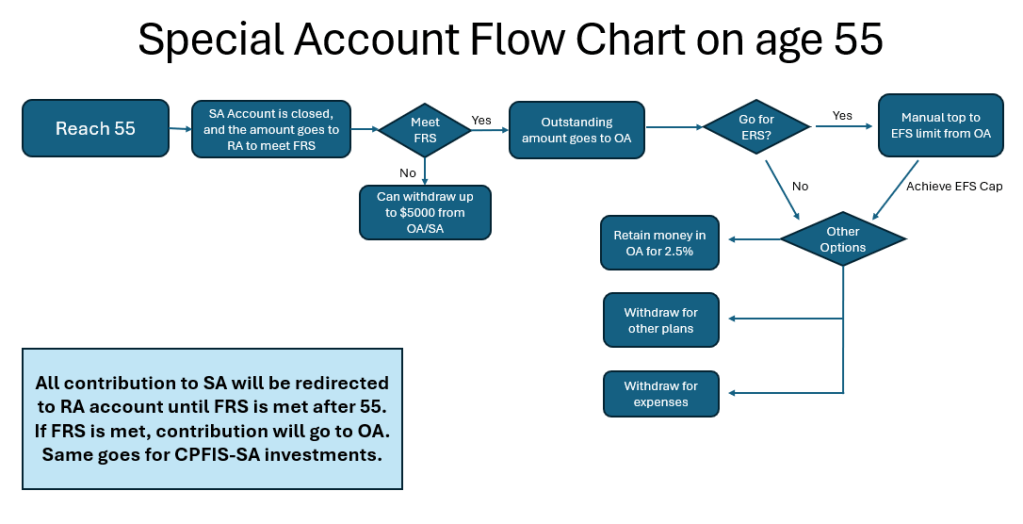

Closure of the Special Account for Members Aged 55 and Above

Starting in January 2025, the CPF Special Account (SA) will be closed for members aged 55 and above. Although the exact date is yet to be confirmed, the transition process has been outlined:

- Funds in SA will be transferred to the CPF Retirement Account (RA) until the member reaches the Full Retirement Sum (FRS).

- Any remaining funds beyond the FRS will be transferred to the CPF Ordinary Account (OA).

Members will then have the following options:

- Withdraw funds from OA

- Manually topping-up the (RA) to achieve the Enhance Retirement Sum (ERS)

- Retain the funds in the OA to earn an interest rate of 2.5%

A flow chart is available to illustrate this process:

ERS Limit Increases

Starting 1 January 2025, the Enhanced Retirement Sum (ERS) will increase from three times to four times the Basic Retirement Sum (BRS). This change allows CPF members aged 55 and above to voluntarily top up more to their Retirement Account (RA), enabling them to receive higher monthly payouts during retirement. The new ERS for 2025 will be $426,000.

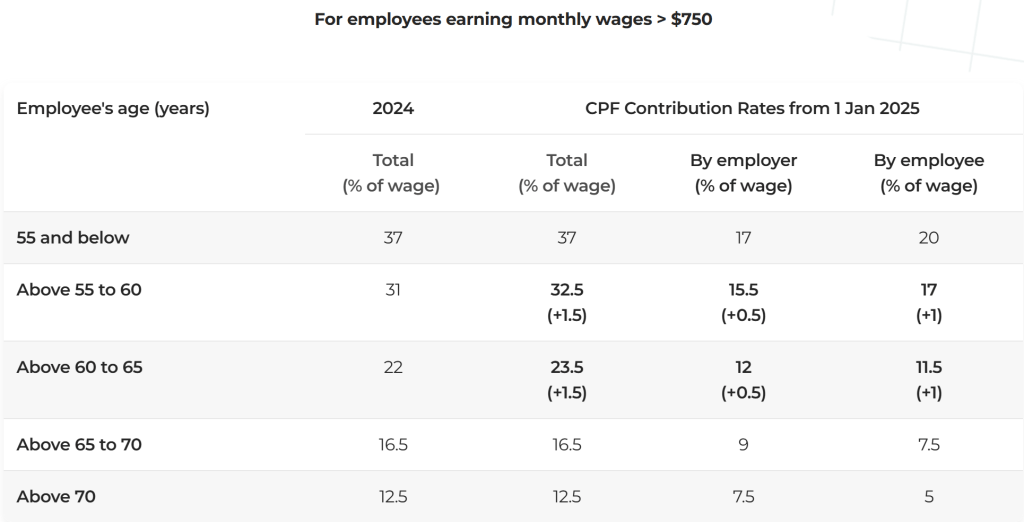

CPF Contribution Rate Increase

Changes to the CPF contribution rates will affect members aged 55 to 65:

- The employer’s contribution will increase by 0.5%.

- The employee’s contribution will increase by 1%.

- For employees earning $750 and below, the employee’s contribution will be gradually phased in.

Increased Wage Ceiling for CPF Contributions

This adjustment has been phased in since 2023 and will continue until 2026. Currently, the wage ceiling for CPF contributions is $6,800, and it will rise by $600 to $7,400 in 2025. This means that if your monthly income is $10,000, only the first $7,400 will be considered for calculating CPF contributions next year.

Stay Prepared for 2025

As we approach 2025, it’s important to stay informed about these changes to your CPF accounts and how they might impact your financial planning. Whether you’re adjusting to the new contribution rates or making decisions about your retirement savings, understanding these updates will help you make the most of your CPF.

If you have any questions or need personalized advice on how these changes could impact you, don’t hesitate to reach out. I’m here to guide you through these updates and ensure that your retirement plans remain on track.

Leave a comment